FDIC-Insured - Backed by the full faith and credit of the U.S. Government

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

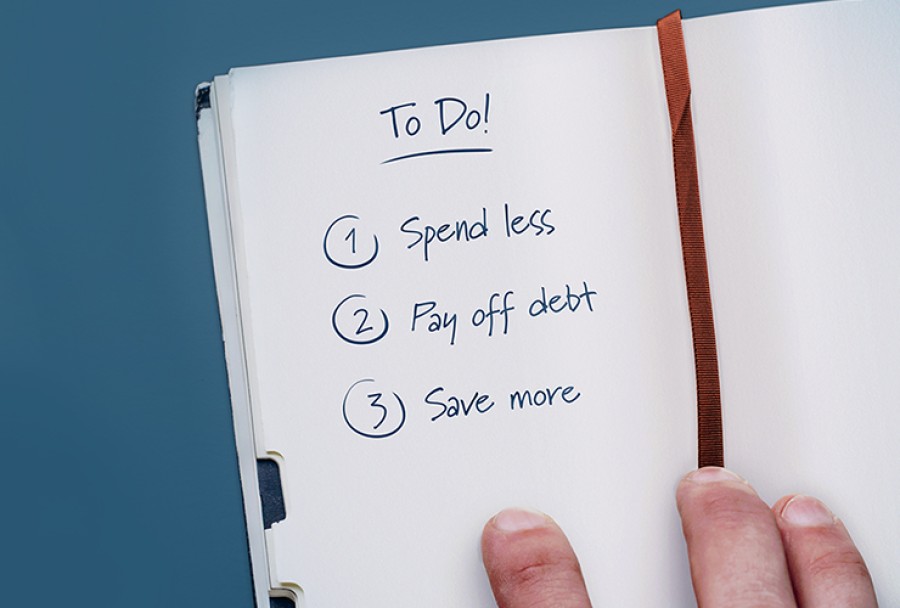

With April showers comes financial literacy! April is Financial Literacy Month, so start your spring cleaning today by taking a look at how you can optimize your financial habits to reach your personal goals.

Let’s take a look at what you can do in each of these areas:

Spend less

There are many easy ways to cut back on your discretionary spending. Just ask yourself a few simple questions: Am I using my gym or tanning salon membership? Do I really need streaming service from multiple sources? Are all these happy hours really making me happy?

Simply revisiting some of these “little” expenses can make a “big” difference. You could easily save between $50–200 a month just by cutting back on things you really don’t need or enjoy.

You can also shop around for better deals on your home and auto insurance and mobile phone plans. Look at opportunities to bundle and ask your providers about any specials or overlooked discounts you may be eligible for.

If you are a homeowner, look into refinancing your mortgage. A general rule of thumb is that an interest rate at least one percentage point lower than your current loan could make refinancing a viable option. The mortgage calculator on southside.com can help you run through different scenarios to see if refinancing makes sense for you.

Pay off debt

Debt is a huge source of anxiety and stress. Paying off those credit cards can be daunting, but it can be done. If you are paying the minimum each month, you won’t make progress. You have to devote resources in order to make headway. If you were able to save money by using some of the ideas above, put those savings to work on your debt.

Did you get a bonus or small raise at the end of the year? Instead of buying something frivolous, invest that money in your financial future and pay down your debt. Take it a step further and consider putting any unexpected windfall or refund you may receive towards credit card debt.

There are two approaches you can consider: paying off the highest interest rate first or tackling your smallest balance first. With either strategy, you’ll get a sense of accomplishment from working towards a goal. Just make sure you continue to make payments on all of your debts even when focusing on one in particular.

Save more

Saving is a habit–and one everyone should have. If you don’t currently have a savings account, open one immediately. You can have a portion of each paycheck diverted via direct deposit. It doesn’t have to be a lot; $20 a week for a year puts $1,000 in reserve.

In a year where you are focusing on spending less and paying off debt, having a robust savings account will make it easier for you to accomplish your goals. When you consider that, according to the Pew Charitable Trust, the average unplanned emergency expense for families is $2,000, the need for a cash reserve becomes clear. With savings to draw from, you won’t have to accumulate more debt when your car breaks down or some other unplanned expense comes along.

The bottom line: by committing to some simple habits, you can greatly increase your financial fitness!

Austin, Texas is flourishing, boasting one of the nation’s most dynamic and resilient economies. Known for its innovative spirit, the...

Fort Worth, Texas continues to evolve as a powerhouse in the commercial landscape, offering both established businesses and new ventures...

Sarah, a recent college graduate, was eager to invest her first paycheck. She'd been following a popular investment influencer online...

The Woodlands, Texas continues to thrive as a premier location for residential and commercial activity. With its strategic planning, high-quality...